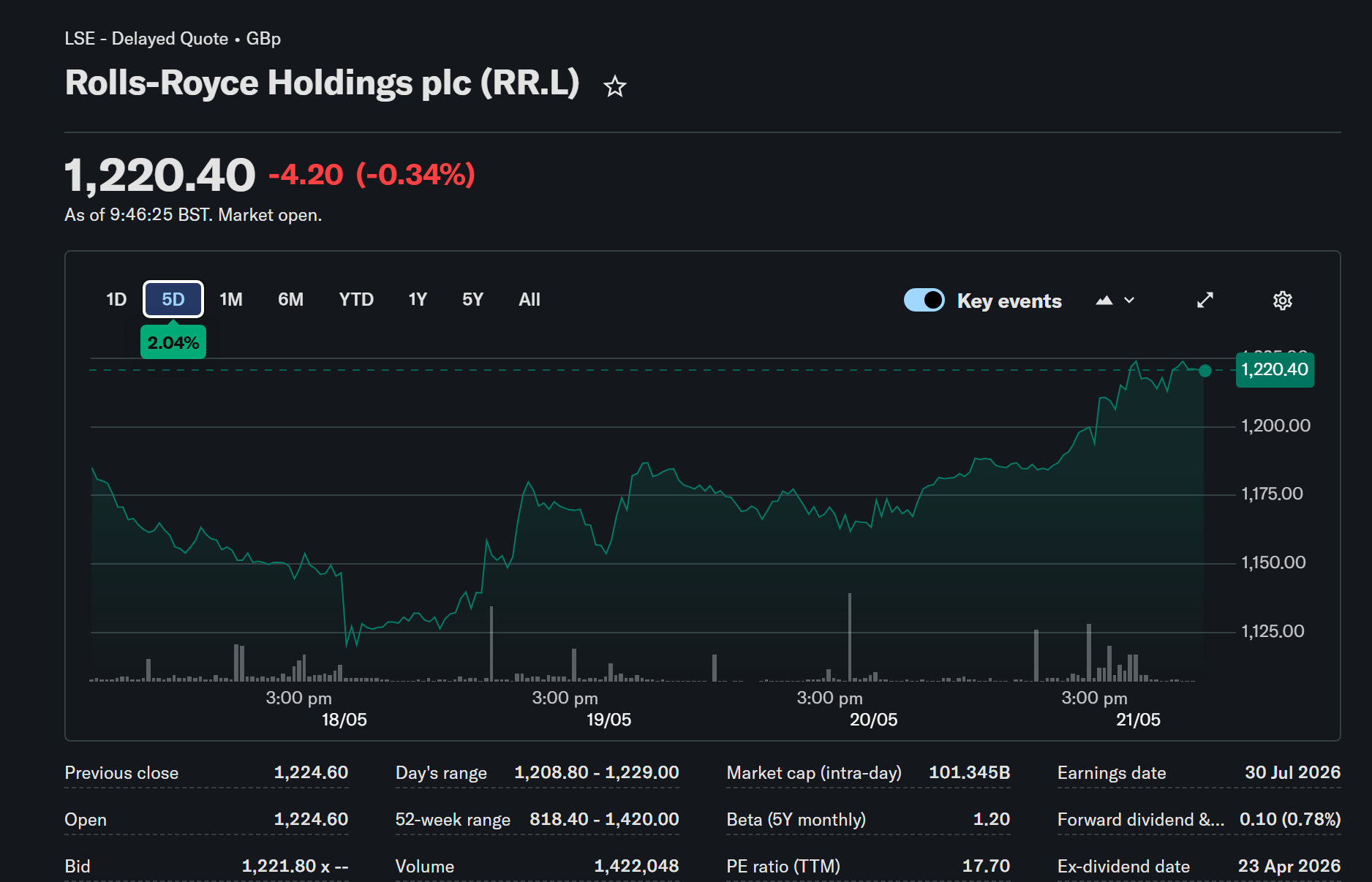

Rolls-Royce (LSE: RR) shares are climbing once more, rising 13% in the past month and pushing the company’s market capitalisation to £112bn.

The FTSE 100 engineering giant has been one of the UK’s most remarkable post-pandemic success stories, with shares up 1,116% over five years.

That extraordinary run would have turned a £10,000 investment into £121,600, illustrating how a single well-timed stock pick can significantly reshape a retirement portfolio.

For much of this year, the prevailing sentiment among investors has been cautious, with many concluding that the strongest gains were already behind the company.

The price-to-earnings ratio had climbed to a dizzying 65 when the market cap hit £100bn, understandably giving investors pause about further upside.

That P/E has since retreated to 44, still elevated by any conventional measure, but less alarming than the peak that rattled confidence earlier in the cycle.

Meanwhile, attention across financial markets has been heavily focused on SpaceX’s public debut, which jumped a further 16.6% on the Monday following its listing on 12 June.

The contrast in sentiment between US and UK investors is striking, with Americans tending to dream big while British investors often apply more caution born of hard experience.

That cultural difference raises a genuine question about whether the market is underestimating Rolls-Royce’s longer-term growth trajectory.

The company’s civil aerospace, defence, and power systems divisions are all performing well simultaneously, a convergence that chief executive Tufan Erginbilgic has capitalised on effectively since taking the helm.

Erginbilgic has also been aggressively pursuing small modular reactor contracts, with deals already secured in the UK, the Czech Republic, and most recently Japan.

Sweden has also signalled strong interest in the technology, further expanding the pipeline of potential SMR agreements for the company.

Erginbilgic estimates the global SMR market will be worth more than $1trn, and has said SMR deals have the “potential” to make Rolls-Royce the most valuable company in the UK.

That claim would require at least a doubling of the current market cap, an ambitious target that underscores both the scale of the opportunity and the risks involved.

SMR technology remains commercially unproven, individual reactors carry a price tag of around £2.2bn each, and Rolls faces intense competition to establish itself in the space.

There are other vulnerabilities too, with its aircraft engines having faced persistent technical issues and United Airlines having recently accused Rolls of “gouging” carriers.

A resolution to conflicts in Iran and Ukraine, while clearly welcome on humanitarian grounds, could also dampen defence spending demand over time.

The possibility that AI investment proves to be a bubble, stalling data centre rollout, represents another risk worth factoring into any assessment of the shares.

Even accounting for all of those headwinds, the combination of Erginbilgic’s leadership, the SMR pipeline, and the company’s strong divisional performance makes Rolls-Royce shares worth serious consideration at current levels.