BAE Systems shares have fallen sharply in recent months, dropping 23% since March and sitting just under 1,800p as analysts point to significant upside ahead.

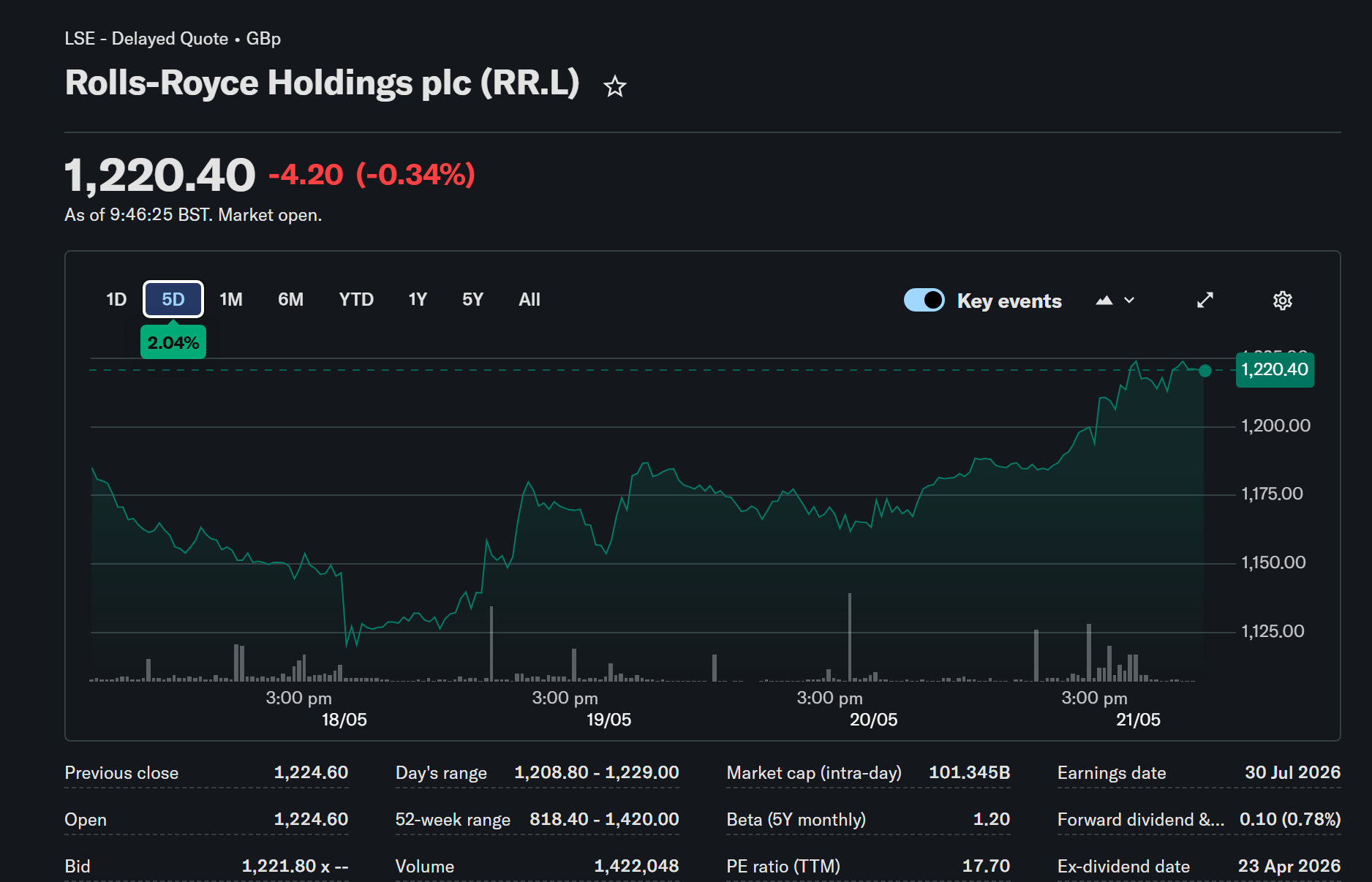

By contrast, Rolls-Royce shares have surged 14% in just two weeks, pushing the one-year return to around 55%, though analyst price targets now sit just 3.5% above current levels.

That gap in projected returns has drawn attention to BAE Systems as a potentially more rewarding opportunity for investors looking beyond the near term.

The average 12-month analyst price target for BAE Systems stands at 2,353p, implying a potential gain of around 31% from current levels.

Even the most conservative estimate among analysts covering the stock sits at 2,050p, representing a 14.5% premium to where shares trade today.

Morgan Stanley is the most bullish of the group, placing a price target of 2,662p on the stock, which would represent a gain of almost 50%.

BAE Systems also trades at a significantly lower forward price-to-earnings ratio of 20.5, compared with Rolls-Royce at 34.5, suggesting better relative value at current prices.

Part of the recent share price weakness has been attributed to reports that Moscow may be ready to negotiate an end to the war in Ukraine, potentially reducing the immediate demand for munitions replenishment.

However, the broader structural case for defence spending remains firmly intact, with the United States calling for a $1.5 trillion defence budget and reducing its military commitments to the NATO alliance.

According to Der Spiegel, Washington is cutting assets it would commit to NATO in crisis scenarios, including fighter jets, submarines, warships, and bomber aircraft, which is likely to accelerate European rearmament programmes.

Reports also suggest that Andy Burnham, described as the UK’s “Prime Minister-in-waiting”, plans to boost defence spending beyond what Keir Starmer had already outlined.

Gulf states represent another growth driver, with Saudi Arabia, which accounts for around 10% of BAE’s revenue, hiking defence spending by 26% in the first quarter after Iran launched strikes in the region.

BAE Systems itself noted in May 2026 that “around the world, security threats continue to grow, leading governments to increase defence spending”, adding that this “provides a supportive backdrop for growth over the medium term.”

The company also highlighted “significant opportunities across our business, including space systems, missile and air defence systems, drones and counter drone technology, electronic warfare, combat aircraft, combat vehicles, frigates and submarines.”

BAE’s order backlog has grown to £83.6bn across its operating segments, providing strong long-term earnings visibility given the multi-year and often multi-decade nature of its programmes.

Management expects underlying profits to rise by as much as 11% in 2026, with free cash flow forecast to exceed £6bn between 2026 and 2028.

That cash generation is expected to support dividend growth of between 9% and 12%, with the company having now increased its payout for 22 consecutive years.

The stock currently offers a forward dividend yield of 2.3%, which analysts consider well covered by earnings given the company’s strong order book and revenue visibility.

Taken together, the combination of compressed valuation, a record backlog, rising global defence budgets, and consistent dividend growth makes BAE Systems a compelling case for investors willing to look past near-term geopolitical uncertainty.